Possible robot algorithms.

There are many trading strategies that trade from the index. It is not feasible to introduce you to all of them. Let's talk about this short list:

1. Index one-legged mean reversion arbitrage.

2. Index one-legged trend arbitrage.

3. Index two-legged arbitrage.

4. Inter-exchange index two-legged arbitrage.

5. Index arbitrage.

0. The index collection is still pending.

In each example of a robot, it is assumed that you have already built the index in some way.

1. Took similar assets to the traded asset.

2. Somehow weighted them by price, volume, or equal shares.

3. And then you plan to compare the securities with the index you want to trade.

4. So, here are the options. This article is about that.

1. Index one-legged mean reversion arbitrage.

Trading the components of this index that have deviated from the index, expecting the security to return to the mean.

Example of possible logic:

1. For each security we want to trade, we build a ratio (divide the index by the security) to the index.

2. Apply Bollinger to this ratio.

3. Make trading operations when there are Bollinger breakouts.

2. Index one-legged trend arbitrage.

Look for a security accelerating upwards from the index on a clearly declining market and trade it in LONG, expecting that it has some fundamental idea and the movement will continue.

Example of possible logic:

1. For each security, we want to trade, we create a "chart of the difference between the index and the security with the optimal multiplier." Apply a line of standard deviation above zero to the chart.

2. Buy the security when the standard deviation line crosses from bottom to top (i.e. the security accelerates upwards).

3. Manage the position with a standard trailing stop.

3. Index pair arbitrage.

Build an index of securities in a certain sector and trade extreme deviations of securities from this index for convergence in pairs.

Example of possible logic:

1. Look for acceleration from the index for each security.

2. If we find a pair accelerating from the index in different directions in a short period, and the spread between the securities exceeds a certain %, fix the spread between them by buying the security accelerating downward and selling the security accelerating upward.

3. Exit when the spread narrows to a certain percentage, or the acceleration of the securities towards each other reaches a certain percentage over a certain period.

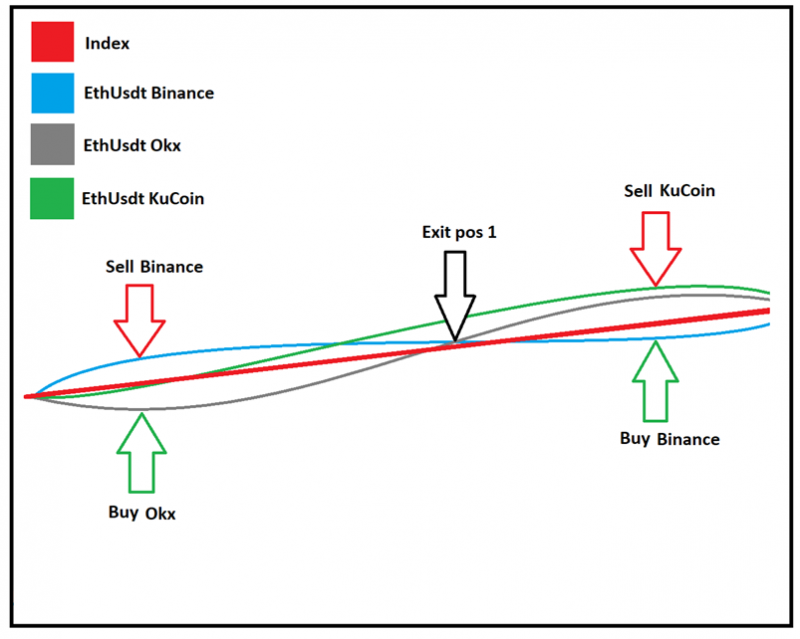

4. Inter-exchange index pair arbitrage.

Build an index of one type of asset traded on different exchanges and trade extreme deviations of securities from this index for convergence in pairs.

Example of possible logic:

1. Look for acceleration from the index for each security.

2. If we find a pair accelerating from the index in different directions in a short period, and the spread between the securities exceeds a certain %, fix the spread between them by buying the security accelerating downward and selling the security accelerating upward.

3. Exit when the spread narrows to a certain percentage or the acceleration of the securities towards each other reaches a certain percentage over a certain period.

5. Index arbitrage.

Trade two indexes relative to each other, as in pair trading, but simultaneously enter all securities included in these indexes. For example, you can build an index of companies in the oil-producing sector in different countries.

Example of possible logic:

1. Build a "chart of the difference with the optimal multiplier" between the indexes. Apply a line of standard deviation above and below zero to the chart.

2. Buy the spread when the standard deviation line crosses (i.e. the indexes accelerate relative to each other).

3. Exit on the reverse signal.

If you have any difficulties or questions, please write to the support chat. Link