About aligning datasets. Trading from index.

We have already discussed missing data in illiquid instruments. Now we need to pay attention to the listing and delisting of securities from the platform. If this issue is not addressed, it will also raise questions about the possibility of testing index arbitrage.

Data synchronicity.

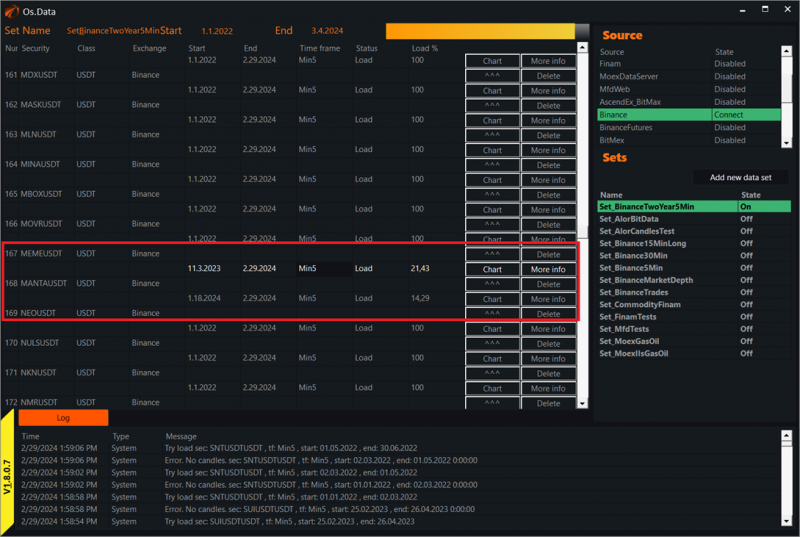

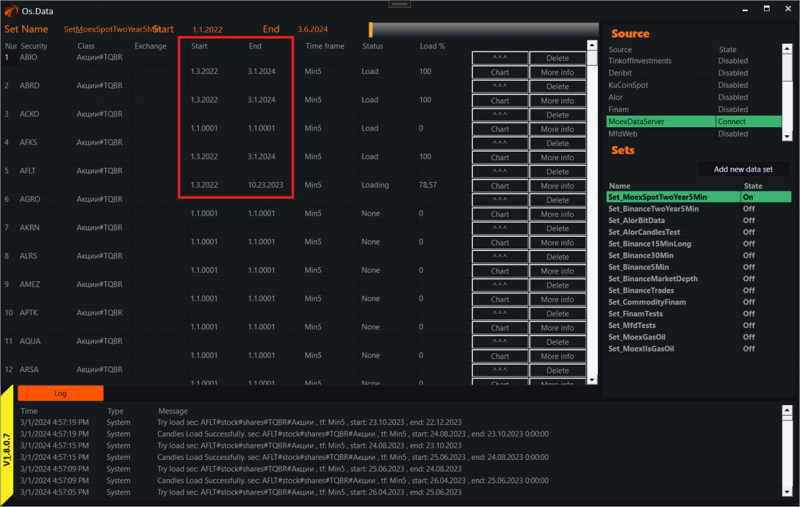

When downloading large datasets and selecting securities based on the principle of "download all," you will inevitably encounter a situation where a ticker has just been introduced to the exchange or has already been removed from trading.

This can be seen in OsData, in the "Load %" column:

All such instruments need to be removed from the dataset.

Also, attention should be paid to the "Start" and "End" columns.

The dates in them must match for all instruments. If you download 300 securities and at least one of them starts two weeks later. Normal tests will start two weeks later than the time of the other 299 securities.

Be careful!

If you have any difficulties or questions, please write to the support chat. Link

OsEngine: https://github.com/AlexWan/OsEngine